A Safe Withdrawal Rate (SWR) is a way to determine how much you can spend in retirement and never go broke. Safe Withdrawal Rates are usually reflected as a percentage of your spendable net worth.

While most people in the FIRE movement recommend a 4% SWR, this may actually be too high for some people. Utilizing a 4% rate requires a stock heavy portfolio and some luck to ensure you’ll never go broke.

Meanwhile a 3% SWR virtually guarantees that you’ll never run out of money, no matter what age you decide to retire.

Why your Safe Withdrawal Rate is important

A good SWR ensures you won’t go broke in retirement. After all, the last thing any retiree wants is to run out of money before they die.

This number drives not only the amount that you need to save for retirement, but also the amount that you can safely spend during these golden years.

Determining a SWR

Safe Withdrawal Rates usually range from 3-5%, with 4% being the most common.

The 4% rule is usually applied by most people in the FIRE movement. This number is cited all over the place. For years, retirement experts have been eoching that 4% is the ideal withdrawal rate for retirees. I’m not going to argue against this, but just provide a word of caution for those following the 4% rule.

The 4% rule was created for people retiring at 65. Does that sound like you? Nope? Me neither.

For people planning to retire early and spend 40 or 50 years in retirement, 4% may prove to be too low. And the worst thing about it, is that you may not realize it’s too low until your 20 years into retirement. What do you do then? Go back to work? Yuck.

Fidelity advices 4% to 5% at full retirement age

When initially researching this topic, I was a little surprised to see that Fidelity recommends a 4% to 5% withdrawal rate (plus adjustments for inflation). This “sustainable withdrawal rate” varies based on your circumstances. And as you may guess, it doesn’t account for early retirement.

Some assumptions Fidelity makes are:

- You live until your 95

- If you have health issues that may compromise your life expectancy, this may be too conservative for you. Even as a healthy person, this still sounds pretty conservative to me. I personally don’t know anyone who’s lived to 95.

- You have a 90% success rate which is a relatively “strong plan”.

- I agree that 90% is a strong plan. But following Fidelity’s model, it seems like 1 out of every 10 retirees may run out of money before they die. I just don’t want to be in the last 10%, and I imagine you don’t want to be either.

Fidelity also assumes that you don’t retire early. If you look at their numbers, their rates vary based on your retirement horizon. In other words, the longer you plan to spend in retirement, the lower your SWR should be. This is not a great model for those planning to FIRE.

In their example, they outline a 4.9% withdrawal rate for someone retiring at 70, and 4.3% withdrawal rate for someone retiring at 60.

This makes perfect sense. The earlier you retire, the more years you’ll have to live without an income. Said another way, the longer your retirement, the more likely you are to run out of funds.

Retirees aren’t just living off money earned by their investments. They’re also selling investments over time. Therefore if you live too long, there comes a point where you may have sold all your investments.

The 4% rule

As I mentioned before, standard retirement advice is to aim for a 4% SWR. You’ll find this guidance from a number of sources, including investment articles, financial planners and most FIRE bloggers. The thing is, this rule comes with a number of limitations.

4% shouldn’t apply to early retirement

As we just discussed, the timing of when you retire can significantly impact your SWR. And most people who follow FIRE, retire well before they reach 65. So if 4% is the rule that financial experts are telling 65 year-old retirees to follow, it seems like it should be lower for those who retire early.

4% requires stock heavy portfolios

When the 4% rule was first created, it was applied to 60/40 stock to bond portfolios. (60% stock and 40% bonds). In today’s market, with a rising stock market and small bond yields, I’ve seen this rule applied to both 80/20 and 100% stock portfolios. These types of allocations carry a lot of risk.

Are you comfortable keeping the bulk of your investments in the stock market, no matter what happens? If not, the 4% rule may be too risky for you.

Riding out down markets

Every now and then the stock market crashes. Most recent crashes occured in 1987, 2000, 2008 and 2020. Sometimes prices bounce right back (like in 1987 and 2020). Other times there is a prolonged bear market where prices don’t recover for years (and even decades).

Over long periods of time the market has had more good years than bad. Meaning that if you keep invested through the down years, you’ll eventually make your losses back. On average, the stock market has returned about 10% a year over the last century, so if you can stomach the bad years, it’s not a bad place to keep your savings.

A potential issue here is assuming that you’ll ride out the crashes. Most people don’t. They see large losses in their portfolios, and begin to sell, even if they know they shouldn’t. Most people prefer the safety of cash or bonds when the stock market is dropping, and it’s hard to blame them.

Today’s financial markets are not normal

When you look at the current financial markets, you’ll find:

- A stock market that doubled over the last 7 years

- Housing prices hitting new highs every month

- Interest rates at historical lows

- Inflation reaching its highest point in a decade

- Bitcoin hitting $65,000 (as of May)

How does this affect the 4% rule?

If you’re FIRE-ing today at the age of 45, your assets need to last for about 40 years of retirement. The current market environment could make that tricky. Financial experts have warned that we’re living in very unique times, and bull markets rarely last this long.

While no one can predict the future, you may want to consider the risks that exist in today’s market.

SWR for FIRE

As you read above, the 4% rule may be a little too aggressive for those pursuing FIRE, and there are a number of models that support this. World renowned economists and financial planners have been studying this for years, and many agree that 4% is too high a number for some retirees. Those retiring at the wrong time (like right before a market crash or during high periods of inflation) could really struggle later in life if they choose to follow this rule.

Applying a 3% rule for FIRE

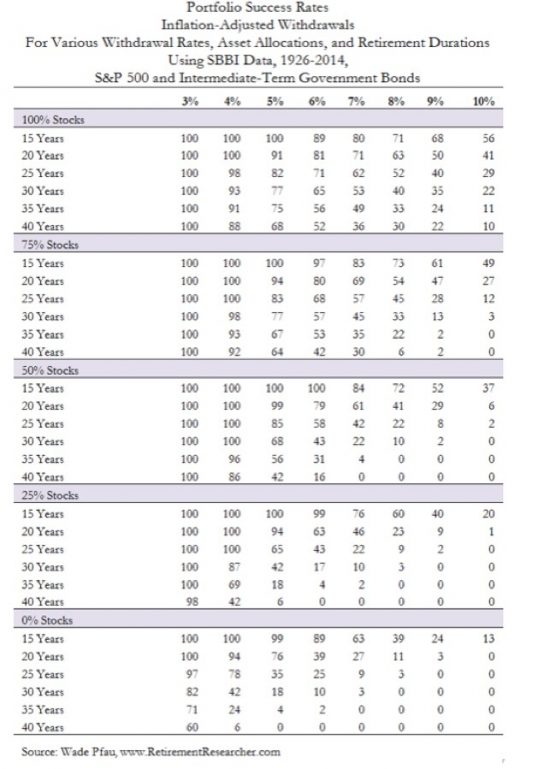

3% sounds close to 4%, but that one extra percentage point can make a world of difference. Using a 3% SRW is much more conservative. In fact a number of projections show that if someone pursuing FIRE uses a 3% rate, they will never run out of money.

As you can see in the table above, it’s important to have a balanced portfolio. It’s also important to keep your SWR low. Most people will have success following the 4% rule, but everyone should fine using a 3% SWR no matter when you retire or how long you’ll live.

Planning to Chubby FIRE

Chubby FIRE is about retiring with a healthy net worth (usually between $2.5m to $7.5m). With this much wealth, keeping your spending between 3% and 4% a year shouldn’t be a struggle.

3% is the more conservative approach, and we recommend that you try to keep your SWR in that range for at least the first few years of retirement. Odds are your investments will grow at a rate of greater than 3%, and as the years pass, you’ll be able to spend more because your net worth is growing.

You’ll also be able to increase your SWR as you age (if you choose) as you’ll be spending less years in retirement. There is a big difference between a 30 year and 40 year time horizon. The less years you plan to spend, the more certainty there is that your funds will last.

Not necessarily a comment on this specific article, but a general comment that your blog is great. As someone who is getting closer every day to ‘chubby fire’ (NW = bottom 1/3 of your definition, top 1/4 of reddit’s definition), it’s always good to have as much reference info as possible to back up my gut and my math :). Nice job.